How expensive can / must I sell my services or products? What costs are actually incurred in the provision of services? How can I improve in the provision of services? Where are critical cost drivers and unused potentials? In order to be able to answer such questions, a new method of controlling has emerged: activity-induced costing – it pursues the goal of creating more transparency about costs (and their distribution). Activity-induced costing is becoming more and more prevalent in practice, as classic cost accounting systems can no longer provide the appropriate answers, e.g. for a differentiated pricing policy. We inform you compactly

- about the goals and basics of process costing as well as about process costs and process cost drivers

- how the use of Process Mining helps to obtain automated transparency about process costs

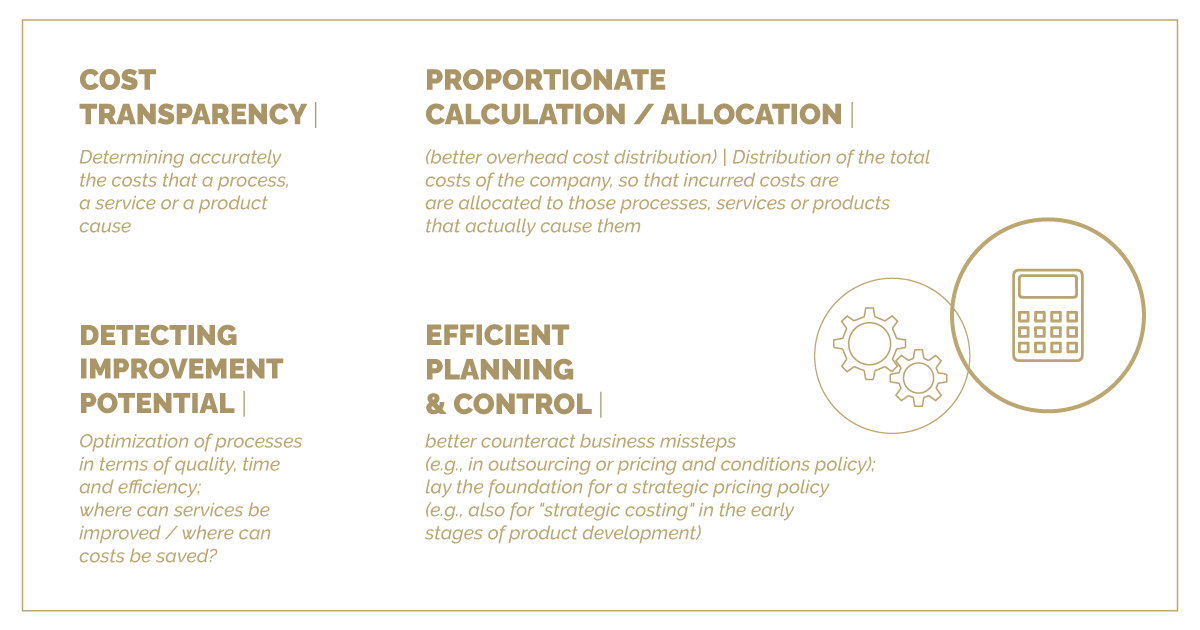

Goals of activity-induced costing

Activity-induced costing examines internal company processes – especially with regard to overhead costs. The most important objectives here are (1):

Goals of activity-induced costing

To understand how you can achieve these goals, a little basic knowledge follows.

What are process costs?

Process costs are those costs that can be attributed to operational procedures (business processes) and their activities. Put simply: those costs that are caused by processes and their work steps. Process costs form the basis of activity-induced costing.

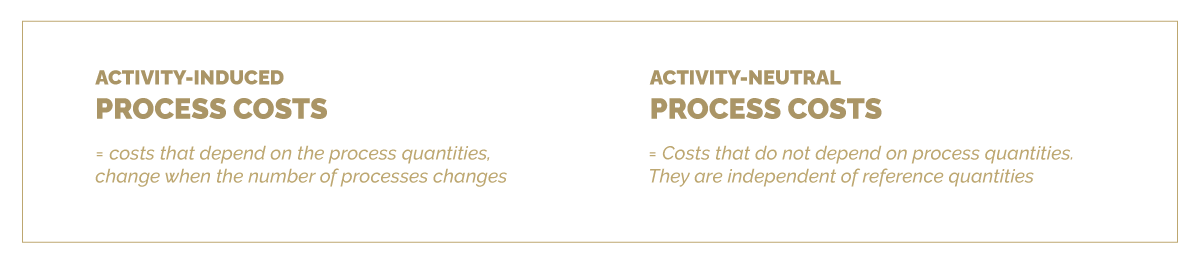

There are two different types of process costs:

Types of process costs

We have found a nice example for the cost center purchasing for you (2):

- In the purchasing cost center, invoices are checked, among other things. The costs of the "check invoices" process depend on the number of invoices to be checked. Thus, they are activity-induced costs.

- The situation is different for the costs incurred by the head of the purchasing cost center. These costs do not depend on the number of invoices to be checked and are therefore activity-neutral costs.

Activity-neutral process costs are therefore independent of the cost drivers claimed for the process. For the actual, activity-induced process costs, on the other hand, the cost drivers have a key role.

What is a cost driver?

- The cost driver of a process is a quantifiable, measurable variable for the result of this process (output / process quantity).

- The cost driver is a measure of resource consumption and thus of the level of costs incurred by this process.(3)

For activity-induced costing, this means that a cost driver is the reference value that is used to allocate a portion of the overhead costs to the cost objects according to their cause. With cost drivers, or process cost rates, the costs charged to the end products are more accurately represented. (4)

Examples of cost drivers

- Number of orders in the sub-process "Edit orders"

- Number of training days for the sub-process "Plan courses"

- Number of company vehicles for the sub-process "Manage leasing contracts"

- Number of customer complaints for the sub-process "Edit complaints"

The analysis of cost drivers is a central element of activity-induced costing (3). The process analysis technology Process Mining can support you in this task and challenge.

You don't know yet where to start with the topic of activity-induced costing? You can find a checklist with helpful questions in our Specialist Portal.

Automated analysis and simulation with Process Mining

With the introduction of activity-induced costing, a precise analysis of the activities and processes in the individual subareas is necessary (5). Process Mining, an innovative technology for automated analysis of actual process flows in IT systems, can simplify and accelerate the analysis of process costs many times over. Process Mining enables:

- Automated identification of process cost drivers

- Root cause analysis for process cost drivers

- Ad-hoc analysis of process costs

- Analysis of allocation in critical events

- Simulation of effects

- Potential analysis

"As a business economist and controller, I naturally also see [in Process Mining technology] the potential to carry out an evaluation of processes more easily and effectively within the framework of activity-induced costing, since the relevant data can be generated on the system side and linked to the business management tools."

(Prof. Dr. Reinhard Rupp, Professor & Certified Public Accountant)

[The quote was translated from German]

You don't know Process Mining yet? In the Insider Portal ProcessMining BlackBox you will find basic knowledge, expertise, use cases and many helpful infographics to explore and understand.

![]()

ProcessMining Blackbox | The Insider-Portal

We open the black box of process mining for you: Discover the insider portal with exclusive, free information.